BLACK'S EXPLANATION OF NOISE VS INFORMATION

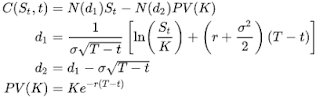

If you are a student of finance, you must have surely heard or seen the infamous Black- Scholes option pricing model. For those who do not about the model, it is basically an equation or a framework by which we can determine the prices of options. Options are one of the major financial derivative security. Fischer Black and Myron Scholes published the paper in 1973 thereby developing the whole derivatives industry. The famous Black- Scholes Option Pricing Model The above is the formula for which Fischer Black is most well known. However, there is another paper he published in 1986 in the Journal of Finance titled "NOISE" . This paper I believe is very much relevant in today's Finance and Economics industry. Actually, if you think about it, it goes beyond just Finance and Economics and can be traced back to every major discipline or event that happens in our world on daily basis. So, let's start by reviewing what Black thinks about NOISE. The reality of the world: Noi...